Thank you for visiting SNEWPapers!

Sign up free

Editorial

April 18, 1803

Alexandria Advertiser And Commercial Intelligencer

Alexandria, Virginia

What is this article about?

Critique of U.S. commissioners' 1802 sale of Bank of the United States stock to Mr. Baring at below-market price, resulting in $119,880 loss, plus unfavorable remittance terms to Amsterdam compared to market exchanges and Manhattan Bank's offer. Defends prior administration against similar accusations.

Merged-components note: The table of exchange rates is spatially embedded within the editorial and contextually part of the discussion on bank stock and financial expediency.

Clipping

OCR Quality

75%

Good

Full Text

From the N. Y. EVENING POST.

PRESIDENT'S MESSAGE.

No. 15.

BANK STOCK.

Having disposed of the question of right it only remains that we examine that of expediency. This has been so fully and satisfactorily discussed by Mr. Bayard, that little else remains than to adapt his remarks to a newspaper essay.

Upon this head, said Mr. Bayard, there are two questions:

1st. Whether the stock was sold for the best price the market afforded?

2d. If not—whether the loss was compensated by any advantage which the government derived from undertakings upon the part of the purchaser?

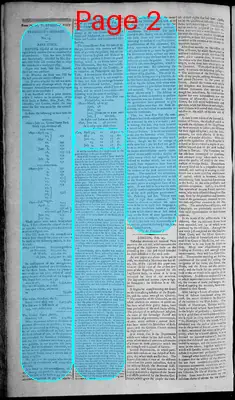

I am furnished with a price current, which I believe to be accurate, of the Bank Stock at Boston, New York, Philadelphia, and London, about the time when the sale was made by the commissioners.

It states the following to have been the prices.

BOSTON.

1802—July 12. United States Bank Stock 150, dividend off.

1802—April 14, 155 1/2

May, 155

June, 154

July, 151

PHILADELPHIA—July 12, 150, dividend off.

1802—Feb. LONDON. 155 1/2

April 7, 155 1/2

27, 158 1/4—advice recd. 4th June.

June 10, 155

July 24, 151

These prices were taken from actual sales. I shall assume the value of the stock at 150, tho' the average price stated would warrant a higher rate.

The sale made by the commissioners was in June 1802, & the payments were to be made at the following periods, in Amsterdam:

1803—1 January, 605,000 guilders.

1st February, 685,000 do.

1st March, 425,000 do.

1st June, 1,425,000 do. stivers.

In consequence of this arrangement, the purchaser received two dividends upon the Bank Stock, before any payment was made on his part, which of course composes part of the profit of his bargain.

The shares sold, 2220, at 150 were worth dols. 1,332,000

The two dividends, at 3 2 dols. upon a share, amounted to 75,480

The value, therefore, the U. States parted with was 1,407,480

The sale was in fact made at 145, and yielded only 1,287,600

The United States plainly, therefore, lost dols. 119,880

When recurrence is had to the times of payment allowed to the purchaser, he may fairly be considered as deriving the benefit of two dividends and an half, upon the stock instead of two, as the payments are protracted by successive instalments, and the last instalment exceeding 1,400,000 guilders, is not payable till June, 1803. But on an estimate undeniable, and as low as any gentleman can contend for, the United States incur a certain loss of dols. 119,880.

We are now to enquire what benefit afforded by the contract will compensate this loss.

It is stated by the commissioners, that Mr. Baring, the purchaser, in consideration of the sale of the stock at 45 per cent. advance,—undertook to pay in Amsterdam, guilders, 3,140,487 16, at the rate of 41 cents the guilder. The result of this engagement, on the part of Mr. Baring, depends upon the course of exchange at the time between the United States and Amsterdam, or between the U. States and London, and London and Amsterdam.

The commissioners state the rate of exchange, between this country and Holland, at 41 cents the guilder, and the exchange between England and Holland to have been 10 guilders 8 stivers per pound sterling, which is 12 stivers below par.

This information, they say, was collected by the Secretary of the Treasury, in an excursion to Philadelphia and New-York. I do not know that the information is incorrect, but it is not complete.

It does not state the exchange between the United States and London. According to communications which I have received, and in which I can confide—the following were the rates of exchange:

Course of Exchange in New-York and Philadelphia, on London

1802—March, 96 to 97

April, 98

May, 99

June, from par to 1 per cent.

July, 1 advance.

In Boston and Salem on London

1802, June 10, 98 per cent.

In London upon Amsterdam.

—Guilders. Stivers.

It will be recollected, that 11 guilders to the pound sterling, is the par of exchange.

Now if the statements which I have made be correct as to the course of exchange, the commissioners so far from having gained any thing for the U. States by the purchase of bills on Holland at 41 cents the guilder, have added to our losses and to the profit of the purchaser of the stock.

In March, April and May, bills on London might have been brought under par—during and subsequent to the same period, bills in London on Amsterdam, might have been purchased also under par. The government therefore might have remitted the instalment of the Dutch debt to Amsterdam, by the way of London, have allowed a commission of one per cent. for the operation, and yet made the remittance at par, and probably below it. This certainly was practicable, when during the period referred to, the average of exchange between the United States and Europe was such, and the exchange between London and Amsterdam more than half per cent. below par. Let me now ask what have the commissioners saved by their contract to compensate the sacrifice of 20 dollars upon each of the 2220 shares of the stock, which they sold.

They have sold our stock considerably below the market price, and have taken bills on Holland, in order to indemnify the United States, at a rate nearly 2 1/2 per cent above par, when the remittance might have been made at par. And it will be remembered at the same time, that a fund producing 8 per cent to the United States, was sacrificed to make this remittance, when there was a dead unproductive capital in the Treasury, which might have been more beneficially employed to accomplish the same purpose.

It is undeniable, that a sacrifice was made of dollars 20 on each share, amounting upon the whole sale to dollars 44,400. The two dividends were also sacrificed, amounting to dollars 75,480, and making an aggregate loss to the U. States of 119,880—and the compensation for this loss is an agreement to remit dolls. 1,287,600, to Amsterdam, for a premium of 2 1/2 per cent amounting to the sum of dollars 32,190 when even this premium might have been saved, by due attention, and proper management.

This premium paid for the remittance ought to be added to the loss of the United States in the transaction, and will increase it to the sum of 152,070 dol's.

The excuse for this sacrifice is a speculative suggestion of the commissioners, that if the government had come into the market in order to purchase bills to the amount of the instalment to be paid in Holland, their demand must have raised the price of bills greatly above par.

But why was not the experiment made, and made at that period of the year when bills were low, and extended to the different commercial towns of the United States? By the report of the commissioners, it would seem that applications were made only to the Bank of the United States and the Manhattan Bank. A contract of this description was not properly the business of any Bank and therefore it could not be expected that any Bank would enter into the contract without a certain prospect of extraordinary profit.

The Bank of the U. States would have nothing to do with the business, & the Manhattan bank offered to make the remittance at 43 cts, the guilder.

—This offer I will show presently, was more advantageous to the government than the one accepted. But what I consider a just ground of complaint against the conduct of the commissioners, is that more industry was not employed to purchase bills with the idle money in the Treasury in our different trading towns. Considering the large remittances annually made to England, the demand of the government could not have materially affected the market, if a competition had been excited But it would seem as if a veil of secrecy had been thrown over the transaction, and I believe I am warranted in saying, that scarcely a merchant in the U. States was informed of the treaty with Mr. Baring until it was completed.

It will now be shewn, that the terms offered by the Manhattan Bank were more beneficial than those acceded to by the government. A very short statement demonstrates the position. The profit allowed to Mr. Baring was 20 dollars on each bank Share and two dividends—amounting to the sum of 119,880 dollars.

In consideration of this allowance, Mr. Baring undertook to pay in Amsterdam 1,287,600 dollars at 41 cents the guilder.

The Manhattan Bank, without any other profit, offered to pay the same sum in Amsterdam at 43 cents the guilder. The difference is two cents the guilder, which is less than 5 per cent. But calculating the difference at 5 per cent. it amounts only to the sum of 64,380 dols. The profit allowed to Mr. Baring was 119,880 dols. As the Manhattan Bank offered to take the contract at 64,380 dollars, their terms were of consequence 55,500 dollars lower than those accepted. Why was this sum of money thrown away? The solidity of the Bank, or their competency to perform the operation was not doubted. And yet the government have preferred to give 55,500 dollars more than the Bank demanded, to an individual to undertake to make the remittance.

Thus, we have seen that the commissioners have made a sale which they were not warranted by any law to make; and in making this sale, they have incurred a certain loss of more than One Hundred Thousand Dollars. It is not our intention to say that the Secretary of the Treasury has been absolutely corrupt in this transaction; though we fix the charge of waste upon him: yet we shall not go so far as to attribute it to fraud. Because the former administration merely appropriated to one public object a surplus of public money which had originally been destined to another object, but was not wanted, their reputations have been assailed by the party now in power with all the violence of the most unrestrained calumny. The exercise of this discretionary power although attended with no loss to the Treasury, was branded in the democratic prints as a frightful scene of iniquity. It was said to be a wanton waste of public treasure unparalleled in the history of the most profligate government."

Mr. Pickering and Mr. Wolcott were called "high state criminals." We should be ashamed to imitate our opponents so far as to apply such language even to the transaction before us; although it is one which charity can at best defend only on the score of utter ignorance of our markets in a foreigner, who to say the best of it, has been very injudiciously and improperly, placed at the head of the American administration.

(To be Continued.)

PRESIDENT'S MESSAGE.

No. 15.

BANK STOCK.

Having disposed of the question of right it only remains that we examine that of expediency. This has been so fully and satisfactorily discussed by Mr. Bayard, that little else remains than to adapt his remarks to a newspaper essay.

Upon this head, said Mr. Bayard, there are two questions:

1st. Whether the stock was sold for the best price the market afforded?

2d. If not—whether the loss was compensated by any advantage which the government derived from undertakings upon the part of the purchaser?

I am furnished with a price current, which I believe to be accurate, of the Bank Stock at Boston, New York, Philadelphia, and London, about the time when the sale was made by the commissioners.

It states the following to have been the prices.

BOSTON.

1802—July 12. United States Bank Stock 150, dividend off.

1802—April 14, 155 1/2

May, 155

June, 154

July, 151

PHILADELPHIA—July 12, 150, dividend off.

1802—Feb. LONDON. 155 1/2

April 7, 155 1/2

27, 158 1/4—advice recd. 4th June.

June 10, 155

July 24, 151

These prices were taken from actual sales. I shall assume the value of the stock at 150, tho' the average price stated would warrant a higher rate.

The sale made by the commissioners was in June 1802, & the payments were to be made at the following periods, in Amsterdam:

1803—1 January, 605,000 guilders.

1st February, 685,000 do.

1st March, 425,000 do.

1st June, 1,425,000 do. stivers.

In consequence of this arrangement, the purchaser received two dividends upon the Bank Stock, before any payment was made on his part, which of course composes part of the profit of his bargain.

The shares sold, 2220, at 150 were worth dols. 1,332,000

The two dividends, at 3 2 dols. upon a share, amounted to 75,480

The value, therefore, the U. States parted with was 1,407,480

The sale was in fact made at 145, and yielded only 1,287,600

The United States plainly, therefore, lost dols. 119,880

When recurrence is had to the times of payment allowed to the purchaser, he may fairly be considered as deriving the benefit of two dividends and an half, upon the stock instead of two, as the payments are protracted by successive instalments, and the last instalment exceeding 1,400,000 guilders, is not payable till June, 1803. But on an estimate undeniable, and as low as any gentleman can contend for, the United States incur a certain loss of dols. 119,880.

We are now to enquire what benefit afforded by the contract will compensate this loss.

It is stated by the commissioners, that Mr. Baring, the purchaser, in consideration of the sale of the stock at 45 per cent. advance,—undertook to pay in Amsterdam, guilders, 3,140,487 16, at the rate of 41 cents the guilder. The result of this engagement, on the part of Mr. Baring, depends upon the course of exchange at the time between the United States and Amsterdam, or between the U. States and London, and London and Amsterdam.

The commissioners state the rate of exchange, between this country and Holland, at 41 cents the guilder, and the exchange between England and Holland to have been 10 guilders 8 stivers per pound sterling, which is 12 stivers below par.

This information, they say, was collected by the Secretary of the Treasury, in an excursion to Philadelphia and New-York. I do not know that the information is incorrect, but it is not complete.

It does not state the exchange between the United States and London. According to communications which I have received, and in which I can confide—the following were the rates of exchange:

Course of Exchange in New-York and Philadelphia, on London

1802—March, 96 to 97

April, 98

May, 99

June, from par to 1 per cent.

July, 1 advance.

In Boston and Salem on London

1802, June 10, 98 per cent.

In London upon Amsterdam.

—Guilders. Stivers.

It will be recollected, that 11 guilders to the pound sterling, is the par of exchange.

Now if the statements which I have made be correct as to the course of exchange, the commissioners so far from having gained any thing for the U. States by the purchase of bills on Holland at 41 cents the guilder, have added to our losses and to the profit of the purchaser of the stock.

In March, April and May, bills on London might have been brought under par—during and subsequent to the same period, bills in London on Amsterdam, might have been purchased also under par. The government therefore might have remitted the instalment of the Dutch debt to Amsterdam, by the way of London, have allowed a commission of one per cent. for the operation, and yet made the remittance at par, and probably below it. This certainly was practicable, when during the period referred to, the average of exchange between the United States and Europe was such, and the exchange between London and Amsterdam more than half per cent. below par. Let me now ask what have the commissioners saved by their contract to compensate the sacrifice of 20 dollars upon each of the 2220 shares of the stock, which they sold.

They have sold our stock considerably below the market price, and have taken bills on Holland, in order to indemnify the United States, at a rate nearly 2 1/2 per cent above par, when the remittance might have been made at par. And it will be remembered at the same time, that a fund producing 8 per cent to the United States, was sacrificed to make this remittance, when there was a dead unproductive capital in the Treasury, which might have been more beneficially employed to accomplish the same purpose.

It is undeniable, that a sacrifice was made of dollars 20 on each share, amounting upon the whole sale to dollars 44,400. The two dividends were also sacrificed, amounting to dollars 75,480, and making an aggregate loss to the U. States of 119,880—and the compensation for this loss is an agreement to remit dolls. 1,287,600, to Amsterdam, for a premium of 2 1/2 per cent amounting to the sum of dollars 32,190 when even this premium might have been saved, by due attention, and proper management.

This premium paid for the remittance ought to be added to the loss of the United States in the transaction, and will increase it to the sum of 152,070 dol's.

The excuse for this sacrifice is a speculative suggestion of the commissioners, that if the government had come into the market in order to purchase bills to the amount of the instalment to be paid in Holland, their demand must have raised the price of bills greatly above par.

But why was not the experiment made, and made at that period of the year when bills were low, and extended to the different commercial towns of the United States? By the report of the commissioners, it would seem that applications were made only to the Bank of the United States and the Manhattan Bank. A contract of this description was not properly the business of any Bank and therefore it could not be expected that any Bank would enter into the contract without a certain prospect of extraordinary profit.

The Bank of the U. States would have nothing to do with the business, & the Manhattan bank offered to make the remittance at 43 cts, the guilder.

—This offer I will show presently, was more advantageous to the government than the one accepted. But what I consider a just ground of complaint against the conduct of the commissioners, is that more industry was not employed to purchase bills with the idle money in the Treasury in our different trading towns. Considering the large remittances annually made to England, the demand of the government could not have materially affected the market, if a competition had been excited But it would seem as if a veil of secrecy had been thrown over the transaction, and I believe I am warranted in saying, that scarcely a merchant in the U. States was informed of the treaty with Mr. Baring until it was completed.

It will now be shewn, that the terms offered by the Manhattan Bank were more beneficial than those acceded to by the government. A very short statement demonstrates the position. The profit allowed to Mr. Baring was 20 dollars on each bank Share and two dividends—amounting to the sum of 119,880 dollars.

In consideration of this allowance, Mr. Baring undertook to pay in Amsterdam 1,287,600 dollars at 41 cents the guilder.

The Manhattan Bank, without any other profit, offered to pay the same sum in Amsterdam at 43 cents the guilder. The difference is two cents the guilder, which is less than 5 per cent. But calculating the difference at 5 per cent. it amounts only to the sum of 64,380 dols. The profit allowed to Mr. Baring was 119,880 dols. As the Manhattan Bank offered to take the contract at 64,380 dollars, their terms were of consequence 55,500 dollars lower than those accepted. Why was this sum of money thrown away? The solidity of the Bank, or their competency to perform the operation was not doubted. And yet the government have preferred to give 55,500 dollars more than the Bank demanded, to an individual to undertake to make the remittance.

Thus, we have seen that the commissioners have made a sale which they were not warranted by any law to make; and in making this sale, they have incurred a certain loss of more than One Hundred Thousand Dollars. It is not our intention to say that the Secretary of the Treasury has been absolutely corrupt in this transaction; though we fix the charge of waste upon him: yet we shall not go so far as to attribute it to fraud. Because the former administration merely appropriated to one public object a surplus of public money which had originally been destined to another object, but was not wanted, their reputations have been assailed by the party now in power with all the violence of the most unrestrained calumny. The exercise of this discretionary power although attended with no loss to the Treasury, was branded in the democratic prints as a frightful scene of iniquity. It was said to be a wanton waste of public treasure unparalleled in the history of the most profligate government."

Mr. Pickering and Mr. Wolcott were called "high state criminals." We should be ashamed to imitate our opponents so far as to apply such language even to the transaction before us; although it is one which charity can at best defend only on the score of utter ignorance of our markets in a foreigner, who to say the best of it, has been very injudiciously and improperly, placed at the head of the American administration.

(To be Continued.)

| 1802, April 30, May | 10 | 16 per L. st. |

| June 11, 25, | 10 | 15 do. |

| July 9, 20, | 10 | 17 do. |

What sub-type of article is it?

Economic Policy

Partisan Politics

What keywords are associated?

Bank Stock Sale

Financial Loss

Government Remittance

Exchange Rates

Commissioners Critique

Dutch Debt

Baring Contract

What entities or persons were involved?

Mr. Bayard

Mr. Baring

Commissioners

Secretary Of The Treasury

Manhattan Bank

Bank Of The United States

Mr. Pickering

Mr. Wolcott

Editorial Details

Primary Topic

Critique Of 1802 U.S. Bank Stock Sale And Remittance Terms

Stance / Tone

Critical Of Commissioners' Financial Decisions And Waste

Key Figures

Mr. Bayard

Mr. Baring

Commissioners

Secretary Of The Treasury

Manhattan Bank

Bank Of The United States

Mr. Pickering

Mr. Wolcott

Key Arguments

Stock Sold At 145 Vs Market 150, Losing $44,400

Two Dividends Sacrificed, Totaling $75,480

Aggregate Loss Of $119,880 Not Compensated

Remittance At 41 Cents/Guilder Vs Possible Par Or Below

Manhattan Bank Offered Better Terms At 43 Cents/Guilder, Saving $55,500

Sale Unauthorized By Law

Criticizes Lack Of Market Exploration And Secrecy