Thank you for visiting SNEWPapers!

Sign up free

Letter to Editor

October 9, 1905

The Spokane Press

Spokane, Spokane County, Washington

What is this article about?

George Mudgett replies to a Spokane Press article accusing him of legal entanglements and benefiting the Security Savings Society while county treasurer. He denies owning a 'tax-shark' society, explains tax assessments on the Belt estate, and defends issuing tax certificates as duty-bound, aiding county finances.

Clipping

OCR Quality

98%

Excellent

Full Text

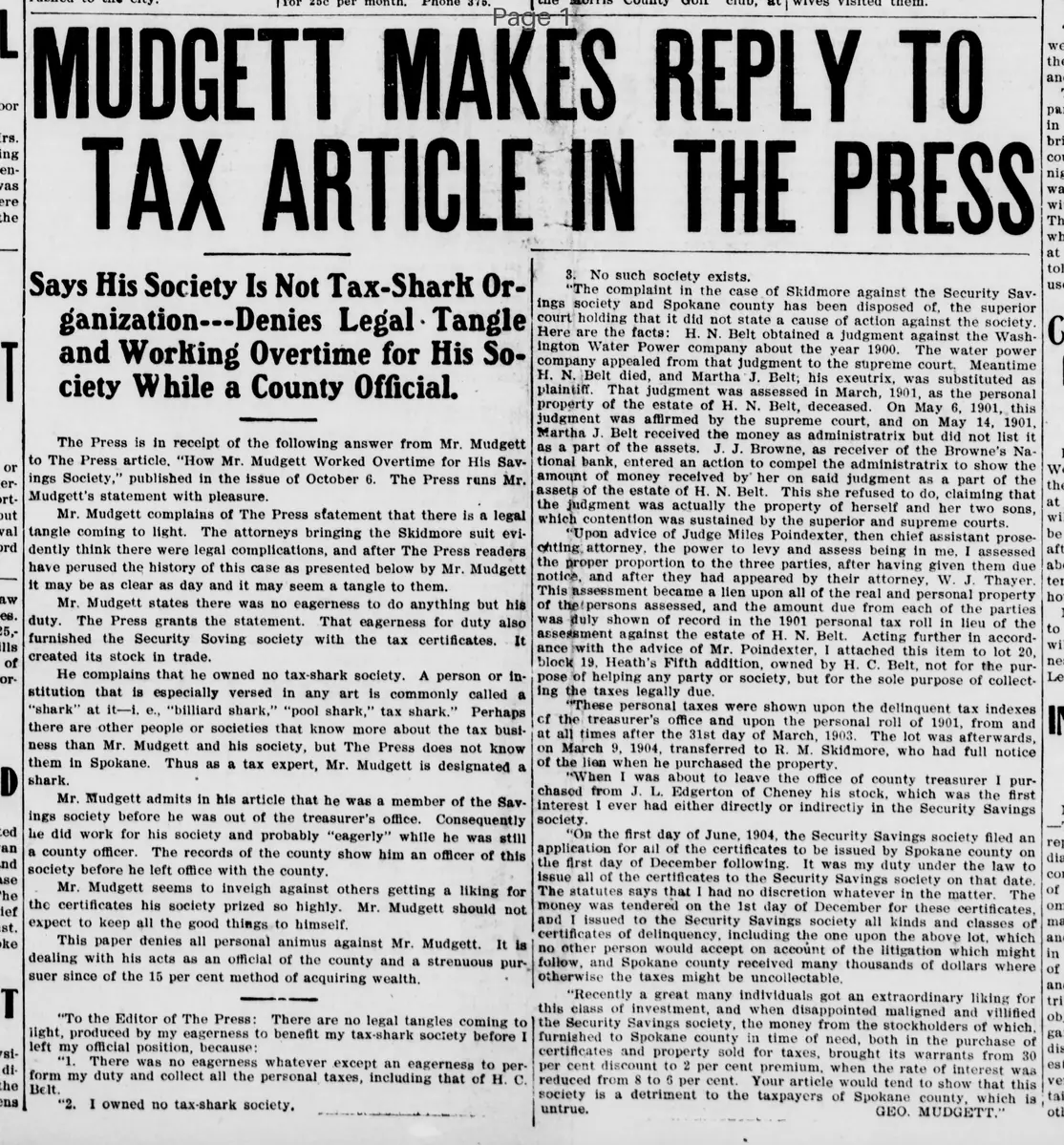

MUDGETT MAKES REPLY TO TAX ARTICLE IN THE PRESS

Says His Society Is Not Tax-Shark Organization—Denies Legal Tangle and Working Overtime for His Society While a County Official.

The Press is in receipt of the following answer from Mr. Mudgett to The Press article, "How Mr. Mudgett Worked Overtime for His Savings Society," published in the issue of October 6. The Press runs Mr. Mudgett's statement with pleasure.

Mr. Mudgett complains of The Press statement that there is a legal tangle coming to light. The attorneys bringing the Skidmore suit evidently think there were legal complications, and after The Press readers have perused the history of this case as presented below by Mr. Mudgett it may be as clear as day and it may seem a tangle to them.

Mr. Mudgett states there was no eagerness to do anything but his duty. The Press grants the statement. That eagerness for duty also furnished the Security Savings society with the tax certificates. It created its stock in trade.

He complains that he owned no tax-shark society. A person or institution that is especially versed in any art is commonly called a "shark" at it—i.e., "billiard shark," "pool shark," tax shark." Perhaps there are other people or societies that know more about the tax business than Mr. Mudgett and his society, but The Press does not know them in Spokane. Thus as a tax expert, Mr. Mudgett is designated a shark.

Mr. Mudgett admits in his article that he was a member of the Savings society before he was out of the treasurer's office. Consequently he did work for his society and probably "eagerly" while he was still a county officer. The records of the county show him an officer of this society before he left office with the county.

Mr. Mudgett seems to inveigh against others getting a liking for the certificates his society prized so highly. Mr. Mudgett should not expect to keep all the good things to himself.

This paper denies all personal animus against Mr. Mudgett. It is dealing with his acts as an official of the county and a strenuous pursuer since of the 15 per cent method of acquiring wealth.

"To the Editor of The Press: There are no legal tangles coming to light, produced by my eagerness to benefit my tax-shark society before I left my official position, because:

"1. There was no eagerness whatever except an eagerness to perform my duty and collect all the personal taxes, including that of H. C. Belt.

"2. I owned no tax-shark society.

"3. No such society exists.

"The complaint in the case of Skidmore against the Security Savings society and Spokane county has been disposed of, the superior court holding that it did not state a cause of action against the society.

Here are the facts: H. N. Belt obtained a judgment against the Washington Water Power company about the year 1900. The water power company appealed from that judgment to the supreme court. Meantime H. N. Belt died, and Martha J. Belt, his executrix, was substituted as plaintiff. That judgment was assessed in March, 1901, as the personal property of the estate of H. N. Belt, deceased. On May 6, 1901, this judgment was affirmed by the supreme court, and on May 14, 1901, Martha J. Belt received the money as administratrix but did not list it as a part of the assets. J. J. Browne, as receiver of the Browne's National bank, entered an action to compel the administratrix to show the amount of money received by her on said judgment as a part of the assets of the estate of H. N. Belt. This she refused to do, claiming that the judgment was actually the property of herself and her two sons, which contention was sustained by the superior and supreme courts.

"Upon advice of Judge Miles Poindexter, then chief assistant prosecuting attorney, the power to levy and assess being in me, I assessed the proper proportion to the three parties, after having given them due notice, and after they had appeared by their attorney, W. J. Thayer.

This assessment became a lien upon all of the real and personal property of the persons assessed, and the amount due from each of the parties was duly shown of record in the 1901 personal tax roll in lieu of the assessment against the estate of H. N. Belt. Acting further in accordance with the advice of Mr. Poindexter, I attached this item to lot 20, block 19, Heath's Fifth addition, owned by H. C. Belt, not for the purpose of helping any party or society, but for the sole purpose of collecting the taxes legally due.

"These personal taxes were shown upon the delinquent tax indexes of the treasurer's office and upon the personal roll of 1901, from and at all times after the 31st day of March, 1903. The lot was afterwards, on March 9, 1904, transferred to R. M. Skidmore, who had full notice of the lien when he purchased the property.

"When I was about to leave the office of county treasurer I purchased from J. L. Edgerton of Cheney his stock, which was the first interest I ever had either directly or indirectly in the Security Savings society.

"On the first day of June, 1904, the Security Savings society filed an application for all of the certificates to be issued by Spokane county on the first day of December following. It was my duty under the law to issue all of the certificates to the Security Savings society on that date. The statute says that I had no discretion whatever in the matter. The money was tendered on the 1st day of December for these certificates, and I issued to the Security Savings society all kinds and classes of certificates of delinquency, including the one upon the above lot, which no other person would accept on account of the litigation which might follow, and Spokane county received many thousands of dollars where otherwise the taxes might be uncollectable.

"Recently a great many individuals got an extraordinary liking for this class of investment, and when disappointed maligned and vilified the Security Savings society, the money from the stockholders of which, furnished to Spokane county in time of need, both in the purchase of certificates and property sold for taxes, brought its warrants from 30 per cent discount to 2 per cent premium, when the rate of interest was reduced from 8 to 6 per cent. Your article would tend to show that this society is a detriment to the taxpayers of Spokane county, which is untrue.

GEO. MUDGETT."

Says His Society Is Not Tax-Shark Organization—Denies Legal Tangle and Working Overtime for His Society While a County Official.

The Press is in receipt of the following answer from Mr. Mudgett to The Press article, "How Mr. Mudgett Worked Overtime for His Savings Society," published in the issue of October 6. The Press runs Mr. Mudgett's statement with pleasure.

Mr. Mudgett complains of The Press statement that there is a legal tangle coming to light. The attorneys bringing the Skidmore suit evidently think there were legal complications, and after The Press readers have perused the history of this case as presented below by Mr. Mudgett it may be as clear as day and it may seem a tangle to them.

Mr. Mudgett states there was no eagerness to do anything but his duty. The Press grants the statement. That eagerness for duty also furnished the Security Savings society with the tax certificates. It created its stock in trade.

He complains that he owned no tax-shark society. A person or institution that is especially versed in any art is commonly called a "shark" at it—i.e., "billiard shark," "pool shark," tax shark." Perhaps there are other people or societies that know more about the tax business than Mr. Mudgett and his society, but The Press does not know them in Spokane. Thus as a tax expert, Mr. Mudgett is designated a shark.

Mr. Mudgett admits in his article that he was a member of the Savings society before he was out of the treasurer's office. Consequently he did work for his society and probably "eagerly" while he was still a county officer. The records of the county show him an officer of this society before he left office with the county.

Mr. Mudgett seems to inveigh against others getting a liking for the certificates his society prized so highly. Mr. Mudgett should not expect to keep all the good things to himself.

This paper denies all personal animus against Mr. Mudgett. It is dealing with his acts as an official of the county and a strenuous pursuer since of the 15 per cent method of acquiring wealth.

"To the Editor of The Press: There are no legal tangles coming to light, produced by my eagerness to benefit my tax-shark society before I left my official position, because:

"1. There was no eagerness whatever except an eagerness to perform my duty and collect all the personal taxes, including that of H. C. Belt.

"2. I owned no tax-shark society.

"3. No such society exists.

"The complaint in the case of Skidmore against the Security Savings society and Spokane county has been disposed of, the superior court holding that it did not state a cause of action against the society.

Here are the facts: H. N. Belt obtained a judgment against the Washington Water Power company about the year 1900. The water power company appealed from that judgment to the supreme court. Meantime H. N. Belt died, and Martha J. Belt, his executrix, was substituted as plaintiff. That judgment was assessed in March, 1901, as the personal property of the estate of H. N. Belt, deceased. On May 6, 1901, this judgment was affirmed by the supreme court, and on May 14, 1901, Martha J. Belt received the money as administratrix but did not list it as a part of the assets. J. J. Browne, as receiver of the Browne's National bank, entered an action to compel the administratrix to show the amount of money received by her on said judgment as a part of the assets of the estate of H. N. Belt. This she refused to do, claiming that the judgment was actually the property of herself and her two sons, which contention was sustained by the superior and supreme courts.

"Upon advice of Judge Miles Poindexter, then chief assistant prosecuting attorney, the power to levy and assess being in me, I assessed the proper proportion to the three parties, after having given them due notice, and after they had appeared by their attorney, W. J. Thayer.

This assessment became a lien upon all of the real and personal property of the persons assessed, and the amount due from each of the parties was duly shown of record in the 1901 personal tax roll in lieu of the assessment against the estate of H. N. Belt. Acting further in accordance with the advice of Mr. Poindexter, I attached this item to lot 20, block 19, Heath's Fifth addition, owned by H. C. Belt, not for the purpose of helping any party or society, but for the sole purpose of collecting the taxes legally due.

"These personal taxes were shown upon the delinquent tax indexes of the treasurer's office and upon the personal roll of 1901, from and at all times after the 31st day of March, 1903. The lot was afterwards, on March 9, 1904, transferred to R. M. Skidmore, who had full notice of the lien when he purchased the property.

"When I was about to leave the office of county treasurer I purchased from J. L. Edgerton of Cheney his stock, which was the first interest I ever had either directly or indirectly in the Security Savings society.

"On the first day of June, 1904, the Security Savings society filed an application for all of the certificates to be issued by Spokane county on the first day of December following. It was my duty under the law to issue all of the certificates to the Security Savings society on that date. The statute says that I had no discretion whatever in the matter. The money was tendered on the 1st day of December for these certificates, and I issued to the Security Savings society all kinds and classes of certificates of delinquency, including the one upon the above lot, which no other person would accept on account of the litigation which might follow, and Spokane county received many thousands of dollars where otherwise the taxes might be uncollectable.

"Recently a great many individuals got an extraordinary liking for this class of investment, and when disappointed maligned and vilified the Security Savings society, the money from the stockholders of which, furnished to Spokane county in time of need, both in the purchase of certificates and property sold for taxes, brought its warrants from 30 per cent discount to 2 per cent premium, when the rate of interest was reduced from 8 to 6 per cent. Your article would tend to show that this society is a detriment to the taxpayers of Spokane county, which is untrue.

GEO. MUDGETT."

What sub-type of article is it?

Persuasive

Informative

Political

What themes does it cover?

Taxation

Politics

Economic Policy

What keywords are associated?

Tax Certificates

Security Savings Society

Spokane County

County Treasurer

Legal Tangle

Belt Estate

Skidmore Suit

Personal Taxes

What entities or persons were involved?

Geo. Mudgett.

To The Editor Of The Press

Letter to Editor Details

Author

Geo. Mudgett.

Recipient

To The Editor Of The Press

Main Argument

there are no legal tangles from eagerness to benefit a tax-shark society; mudgett acted only in duty to collect taxes, owned no such society, and issuing certificates to security savings society was legally required, benefiting spokane county finances.

Notable Details

Denies Ownership Of Tax Shark Society

Explains Belt Estate Tax Assessment In 1901

Skidmore Suit Dismissed Against Society

Purchased Stock In Security Savings Society Before Leaving Treasurer Office

Issued Tax Certificates December 1904 Per Law

Society's Investments Improved County Warrants