Thank you for visiting SNEWPapers!

Sign up free

Editorial

January 4, 1937

The Key West Citizen

Key West, Monroe County, Florida

What is this article about?

Walter E. Spahr critiques the commodity dollar plan, arguing it fails to stabilize prices, disrupts foreign exchange, and offers no advantages over existing credit controls. He emphasizes the importance of price harmony and stable currencies for international trade.

Clipping

OCR Quality

95%

Excellent

Full Text

THE KEY WEST CITIZEN

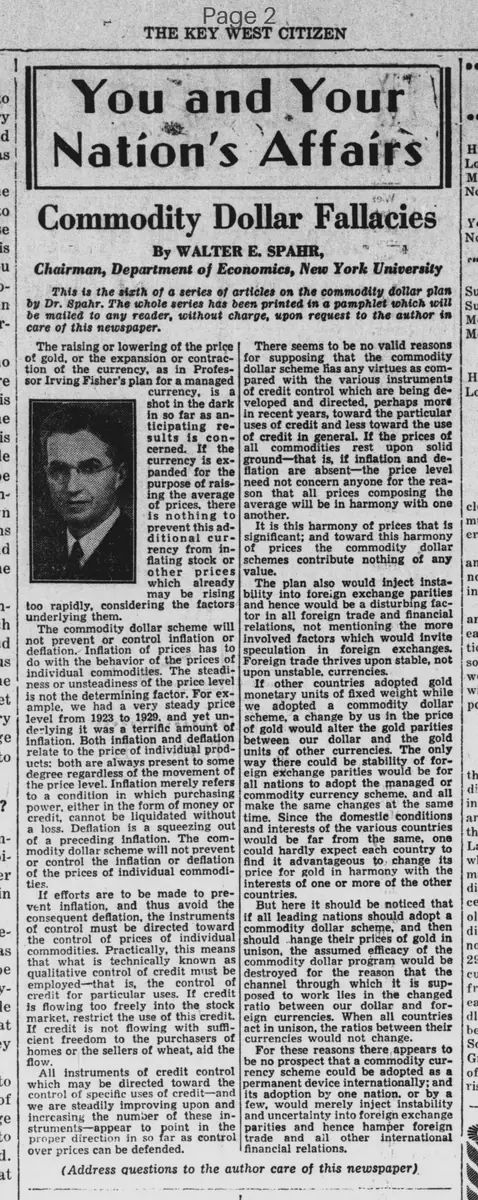

You and Your Nation's Affairs

Commodity Dollar Fallacies

By WALTER E. SPAHR,

Chairman, Department of Economics, New York University

This is the sixth of a series of articles on the commodity dollar plan by Dr. Spahr. The whole series has been printed in a pamphlet which will be mailed to any reader, without charge, upon request to the author in care of this newspaper.

The raising or lowering of the price of gold, or the expansion or contraction of the currency, as in Professor Irving Fisher's plan for a managed currency, is a shot in the dark in so far as anticipating results is concerned. If the currency is expanded for the purpose of raising the average of prices, there is nothing to prevent this additional currency from inflating stock or other prices which may be rising too rapidly, considering the factors underlying them.

The commodity dollar scheme has no virtues as compared with the various instruments of credit control which are being developed and directed, perhaps more in recent years, toward the particular uses of credit and less toward the use of credit in general. If the prices of all commodities rest upon solid ground—that is, if inflation and deflation are absent—the price level need not concern anyone for the reason that all prices composing the average will be in harmony with one another.

It is this harmony of prices that is significant; and toward this harmony of prices the commodity dollar schemes contribute nothing of any value.

The plan also would inject instability into foreign exchange parities and hence would be a disturbing factor in all foreign trade and financial relations, not mentioning the more involved factors which would invite speculation in foreign exchanges. Foreign trade thrives upon stable, not upon unstable, currencies.

If other countries adopted gold monetary units of fixed weight while we adopted a commodity dollar scheme, a change by us in the price of gold would alter the gold parities between our dollar and the gold units of other currencies. The only way there could be stability of foreign exchange parities would be for all nations to adopt the managed or commodity currency scheme, and all make the same changes at the same time. Since the domestic conditions and interests of the various countries would be far from the same, one could hardly expect each country to find it advantageous to change its price for gold in harmony with the interests of one or more of the other countries.

But here it should be noticed that if all leading nations should adopt a commodity dollar scheme, and then should change their prices of gold in unison, the assumed efficacy of the commodity dollar program would be destroyed for the reason that the channel through which it is supposed to work lies in the changed ratio between our dollar and foreign currencies. When all countries act in unison, the ratios between their currencies would not change.

For these reasons there appears to be no prospect that a commodity currency scheme could be adopted as a permanent device internationally; and its adoption by one nation, or by a few, would merely inject instability and uncertainty into foreign exchange parities and hence hamper foreign trade and all other international financial relations.

All instruments of credit control which may be directed toward the control of specific uses of credit—and we are steadily improving upon and increasing the number of these instruments—appear to point in the proper direction in so far as control over prices can be defended.

(Address questions to the author care of this newspaper)

You and Your Nation's Affairs

Commodity Dollar Fallacies

By WALTER E. SPAHR,

Chairman, Department of Economics, New York University

This is the sixth of a series of articles on the commodity dollar plan by Dr. Spahr. The whole series has been printed in a pamphlet which will be mailed to any reader, without charge, upon request to the author in care of this newspaper.

The raising or lowering of the price of gold, or the expansion or contraction of the currency, as in Professor Irving Fisher's plan for a managed currency, is a shot in the dark in so far as anticipating results is concerned. If the currency is expanded for the purpose of raising the average of prices, there is nothing to prevent this additional currency from inflating stock or other prices which may be rising too rapidly, considering the factors underlying them.

The commodity dollar scheme has no virtues as compared with the various instruments of credit control which are being developed and directed, perhaps more in recent years, toward the particular uses of credit and less toward the use of credit in general. If the prices of all commodities rest upon solid ground—that is, if inflation and deflation are absent—the price level need not concern anyone for the reason that all prices composing the average will be in harmony with one another.

It is this harmony of prices that is significant; and toward this harmony of prices the commodity dollar schemes contribute nothing of any value.

The plan also would inject instability into foreign exchange parities and hence would be a disturbing factor in all foreign trade and financial relations, not mentioning the more involved factors which would invite speculation in foreign exchanges. Foreign trade thrives upon stable, not upon unstable, currencies.

If other countries adopted gold monetary units of fixed weight while we adopted a commodity dollar scheme, a change by us in the price of gold would alter the gold parities between our dollar and the gold units of other currencies. The only way there could be stability of foreign exchange parities would be for all nations to adopt the managed or commodity currency scheme, and all make the same changes at the same time. Since the domestic conditions and interests of the various countries would be far from the same, one could hardly expect each country to find it advantageous to change its price for gold in harmony with the interests of one or more of the other countries.

But here it should be noticed that if all leading nations should adopt a commodity dollar scheme, and then should change their prices of gold in unison, the assumed efficacy of the commodity dollar program would be destroyed for the reason that the channel through which it is supposed to work lies in the changed ratio between our dollar and foreign currencies. When all countries act in unison, the ratios between their currencies would not change.

For these reasons there appears to be no prospect that a commodity currency scheme could be adopted as a permanent device internationally; and its adoption by one nation, or by a few, would merely inject instability and uncertainty into foreign exchange parities and hence hamper foreign trade and all other international financial relations.

All instruments of credit control which may be directed toward the control of specific uses of credit—and we are steadily improving upon and increasing the number of these instruments—appear to point in the proper direction in so far as control over prices can be defended.

(Address questions to the author care of this newspaper)

What sub-type of article is it?

Economic Policy

Trade Or Commerce

What keywords are associated?

Commodity Dollar

Managed Currency

Price Stability

Foreign Exchange

Credit Control

International Trade

Gold Standard

What entities or persons were involved?

Walter E. Spahr

Irving Fisher

New York University

Editorial Details

Primary Topic

Critique Of The Commodity Dollar Plan

Stance / Tone

Critical Opposition To Managed Currency Schemes

Key Figures

Walter E. Spahr

Irving Fisher

New York University

Key Arguments

Raising Or Lowering Gold Price Or Currency Expansion Is Unpredictable And May Inflate Speculative Prices.

Commodity Dollar Offers No Advantages Over Targeted Credit Controls.

Price Harmony Is Key, And Commodity Dollar Contributes Nothing To It.

It Injects Instability Into Foreign Exchange Parities, Harming International Trade.

Stability Requires All Nations To Adopt And Change In Unison, Which Is Unlikely Due To Differing Interests.

If All Nations Change In Unison, The Plan's Efficacy Is Destroyed As Currency Ratios Remain Unchanged.

Adoption By Few Nations Would Create Uncertainty In Global Financial Relations.

Better To Improve Instruments For Specific Credit Uses.