Thank you for visiting SNEWPapers!

Sign up free

The Lincoln Times

Lincolnton, Lincoln County, North Carolina

What is this article about?

The new US income tax law effective 1946 provides relief to married individuals with dependents through increased exemptions and reduced rates, exempting many low-income families from taxation and lowering withholdings from wages.

Merged-components note: Tables provide tax data integral to the income tax law article; merged based on reading order sequence and spatial positioning within the article columns.

Clipping

OCR Quality

Full Text

Tax

Law

Means

Savings to

Men

With

Families

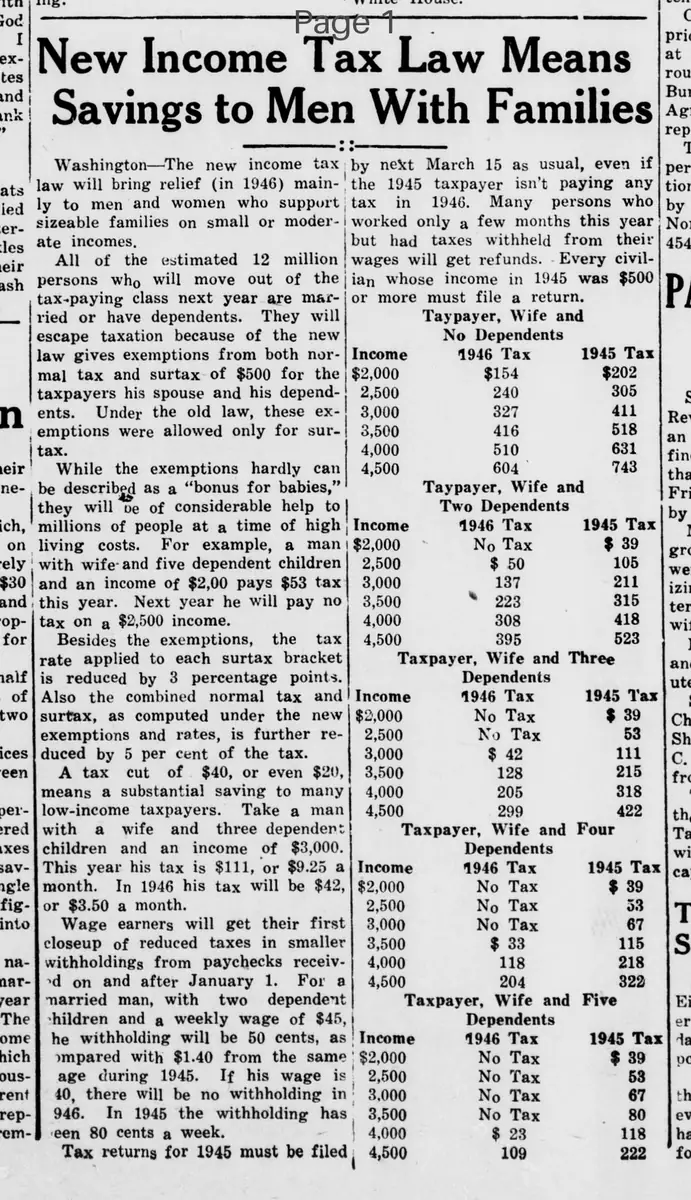

Washington—The new income tax law will bring relief (in 1946) mainly to men and women who support sizeable families on small or moderate incomes.

All of the estimated 12 million persons who will move out of the tax-paying class next year are married or have dependents. They will escape taxation because the new law gives exemptions from both normal tax and surtax of $500 for the taxpayer, his spouse and his dependents. Under the old law, these exemptions were allowed only for surtax.

While the exemptions hardly can be described as a "bonus for babies," they will be of considerable help to millions of people at a time of high living costs. For example, a man with wife and five dependent children and an income of $2,000 pays $53 tax this year. Next year he will pay no tax on a $2,500 income.

Besides the exemptions, the tax rate applied to each surtax bracket is reduced by 3 percentage points. Also the combined normal tax and surtax, as computed under the new exemptions and rates, is further reduced by 5 per cent of the tax.

A tax cut of $40, or even $20, means a substantial saving to many low-income taxpayers. Take a man with a wife and three dependent children and an income of $3,000. This year his tax is $111, or $9.25 a month. In 1946 his tax will be $42, or $3.50 a month.

Wage earners will get their first closeup of reduced taxes in smaller withholdings from paychecks received on and after January 1. For a married man, with two dependent children and a weekly wage of $45, the withholding will be 50 cents, as compared with $1.40 from the same wage during 1945. If his wage is $40, there will be no withholding in 1946. In 1945 the withholding has been 80 cents a week.

Tax returns for 1945 must be filed by next March 15 as usual, even if the 1945 taxpayer isn't paying any tax in 1946. Many persons who worked only a few months this year but had taxes withheld from their wages will get refunds. Every civilian whose income in 1945 was $500 or more must file a return.

Taxpayer, Wife and No Dependents

Income $2,000 2,500 3,000 3,500 4,000 4,500

Taxpayer, Wife and Two Dependents

Taxpayer, Wife and Three Dependents

Income 1946 Tax 1945 Tax

$2,000 No Tax $39

2,500 No Tax 53

3,000 $42 111

3,500 128 215

4,000 205 318

4,500 299 422

Taxpayer, Wife and Four Dependents

Taxpayer, Wife and Five Dependents

| 1946 Tax | 1945 Tax |

| $154 | $202 |

| 240 | 305 |

| 327 | 411 |

| 416 | 518 |

| 510 | 631 |

| 604 | 743 |

| Income | 1946 Tax | 1945 Tax |

| $2,000 | No Tax | $39 |

| 2,500 | $50 | 105 |

| 3,000 | 137 | 211 |

| 3,500 | 223 | 315 |

| 4,000 | 308 | 418 |

| 4,500 | 395 | 523 |

| Income | 1946 Tax | 1945 Tax |

| $2,000 | No Tax | $39 |

| 2,500 | No Tax | 53 |

| 3,000 | No Tax | 67 |

| 3,500 | $33 | 115 |

| 4,000 | 118 | 218 |

| 4,500 | 204 | 322 |

| income | 1946 Tax | 1945 Tax |

| $2,000 | No Tax | $ 39 |

| 2,500 | No Tax | 53 |

| 3,000 | No Tax | 67 |

| 3,500 | No Tax | 80 |

| 4,000 | $ 23 | 118 |

| 4,500 | 109 | 222 |

What sub-type of article is it?

What keywords are associated?

Where did it happen?

Domestic News Details

Primary Location

Washington

Event Date

In 1946

Outcome

tax relief for low to moderate income families with dependents, including exemptions of $500 each for taxpayer, spouse, and dependents from both normal tax and surtax; reduced surtax rates by 3 percentage points; additional 5% reduction on combined tax; smaller wage withholdings starting january 1, 1946; estimated 12 million persons move out of tax-paying class.

Event Details

The new income tax law provides increased exemptions and reduced rates, benefiting married individuals with dependents on small or moderate incomes by allowing many to escape taxation entirely. Examples include a man with wife and five children paying no tax on $2,500 in 1946 versus $53 on $2,000 in 1945; a man with wife and three children paying $42 on $3,000 in 1946 versus $111 in 1945. Wage withholding examples: $45 weekly wage drops from $1.40 to $0.50; $40 weekly from $0.80 to $0. Tax returns for 1945 due March 15, 1946, with refunds possible for those with withholdings.